The allergic rhinitis treatment market is estimated to be valued at US$ 14,916.9 million in 2023 and is expected to exhibit a CAGR of 4.1% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Allergic rhinitis or hay fever is caused when the body's immune system overreacts to allergens like pollen, dust mites, animal dander, or molds in the air. Common symptoms of allergic rhinitis include sneezing, nasal congestion, runny nose, and itchy eyes. The allergic rhinitis treatment market offers various products to manage symptoms like antihistamines, decongestants, nasal strips, immunotherapy, and intranasal corticosteroids. Intranasal corticosteroids are the most effective treatment option for reducing nasal symptoms and are commonly prescribed by doctors as the first line of defense. Market Dynamics: The growing prevalence of allergic diseases globally is a major driver boosting the allergic rhinitis treatment market growth. According to a report by American Academy of Allergy Asthma & Immunology, more than 50 million Americans suffer from allergies every year. Further, rising awareness about treatment options and frequent product innovations are also fueling the market demand. For example, in 2020, Regeneron Pharmaceuticals launched nasal spray REGN-COV2, which is aimed at treating and preventing COVID-19. Additionally, changing lifestyle and pollution levels are increasing the exposure to various allergens and thereby leading to a rising incidence of allergic rhinitis, particularly in urban areas. Segment Analysis The Allergic Rhinitis Treatment Market Size is segmented into medication, immunotherapy and others. Amongst these, the medication segment dominates the market owing to the increasing prevalence of allergic rhinitis across the globe. Medication involves both prescription medications like antihistamines and decongestants and over-the-counter drugs to provide relief from symptoms. The medication segment is further divided into antihistamines, intranasal corticosteroids, leukotriene receptor antagonists and mast cell stabilizers. PEST Analysis Political: Governments across countries are raising awareness about allergic rhinitis through campaigns and increasing insurance coverage for its treatment which is positively impacting the market growth. Economic: Rise in disposable income levels have increased the affordability of advanced treatment options for allergic rhinitis in developing nations, driving the market. Social: Growing incidence of allergic disorders due to changing lifestyle and environmental conditions is increasing the social and economic burden related to allergic rhinitis treatment. Technological: Companies are investing in R&D to develop more effective drugs with novel mechanisms of action and comfortable drug delivery forms like sublingual tablets to improve treatment outcomes. Key Takeaways The global allergic rhinitis treatment market is expected to witness high growth, exhibiting CAGR of 4.1% over the forecast period, due to increasing environmental pollution and adoption of western lifestyles across emerging countries. Regionally, North America accounted for the largest market share in 2021 owing to the presence of major players and continuously rising disease incidence in the US and Canada. Key players operating in the allergic rhinitis treatment market are Merck & Co., Inc., Boehringer Ingelheim International GmbH, AstraZeneca, GSK plc., Johnson & Johnson Services, Inc. Teva Pharmaceutical Industries Ltd., Novartis AG, Mylan N.V., Aytu BioPharma, Inc., Glenmark Pharmaceuticals Ltd, Himalaya Wellness Company, Regeneron Pharmaceuticals Inc., Allergy Therapeutics, Stallergenes Greer, Bayer AG, Dr. Reddy’s Laboratories Ltd, ALK-Abelló A/S, and Revolo Biotherapeutics. Regional analysis shows that the Asia Pacific region is expected to witness the fastest growth during the forecast period due to rising awareness, healthcare infrastructure development and growing expenditure on prescription drugs in China and India. Key players operating in the allergic rhinitis treatment market are focusing on new product launches and partnerships with local players to strengthen their presence in developing markets. For instance, Merck & Co. launched a new digital therapeutics solution Clarify for allergic rhinitis in 2021. Read More: https://www.rapidwebwire.com/allergic-rhinitis-treatment-market-trends/

0 Comments

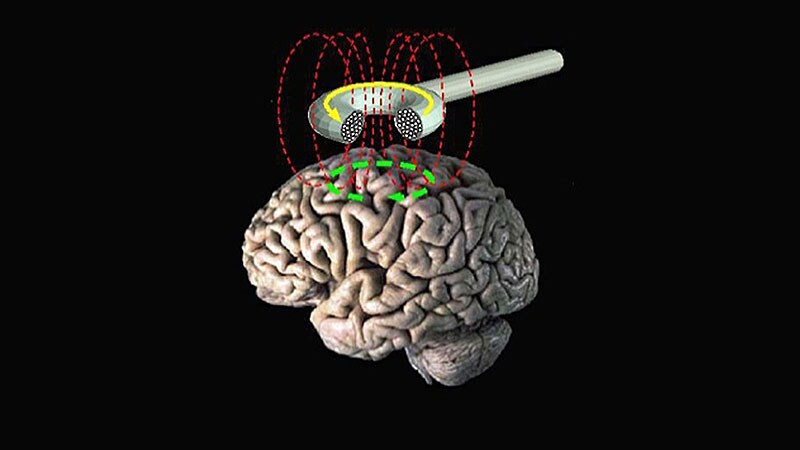

The Anatomic Pathology market is estimated to be valued at US$ 30.16 Bn in 2023 and is expected to exhibit a CAGR of 8.7% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Anatomic pathology refers to the gross and microscopic examination of tissues for the purpose of disease diagnosis. It involves examination of tissues, cells and body fluids using surgical pathology and autopsy or biopsy materials. Anatomic pathologists detect diseases like cancer, infection or inflammation among others through examination of biopsies and surgical specimens. They work closely with oncologists, surgeons, psychiatrists and other physicians to accurately diagnose and evaluate diseases. Anatomic pathology plays a vital role in disease diagnosis and guiding appropriate treatment decisions. Advances in immunohistochemistry, molecular testing and digital pathology are driving market growth. Market Dynamics: Rising prevalence of chronic diseases such as cancer is a major growth driver for the anatomic pathology market. Cancer is one of the leading causes of death worldwide. According to the World Health Organization, cancer burden is expected to grow to 27.5 million new cancer cases and 16.3 million cancer deaths by 2040. Early detection through anatomic pathology examination can significantly improve cancer treatment outcomes. Moreover, increasing demand for personalized medicine and companion diagnostics is propelling the need for advanced diagnostic techniques in anatomic pathology. Growing geriatric population also fuels market growth as risk of cancer and other chronic diseases increases with age. Furthermore, ongoing R&D for development of novel immuno-oncology therapies is reinforcing demand for companion diagnostic tests in anatomic pathology. Market Dynamics: The Global Anatomic Pathology Market is witnessing increasing adoption of digital and automated solutions for pathology diagnosis. Use of digital pathology solutions allows swift and accurate scanning, analyzing and storing of pathology slides. This enables real-time collaboration between pathologists located at different sites. Automated slide scanning also reduces diagnostic errors and improves workflow efficiency. Growing investments by key players to develop advanced automation, imaging, machine learning and AI technologies in pathology are likely to transform the market in the coming years. For instance, Danaher Corporation offers digital pathology scanner called PixelSlide for whole slide scanning and image analysis. Segment Analysis The anatomic pathology market is segmented into instruments, consumables, and services. The consumables segment accounts for the largest share of the market owing to the high frequency of usage of consumables such as reagents, antibodies, probes, and kits for diagnosis. The consumables segment is further divided into histology consumables, immunohistochemistry (IHC) consumables, and cytopathology consumables. Among these, the histology consumables sub-segment dominates the market as histological examination is commonly used in diagnosis of diseases. PEST Analysis Political: Regulations regarding reimbursements and guidelines for disease diagnosis influences the market. Economic: Rising healthcare expenditure in developed countries and booming medical tourism in emerging nations boost market growth. Social: Growing public awareness about early disease diagnosis and increasing prevalence of chronic diseases drive market expansion. Technological: Digital pathology solutions and automation are revolutionizing anatomic pathology through artificial intelligence, machine learning, and workflow optimization. Key Takeaways The global anatomic pathology market is expected to witness high growth, exhibiting CAGR of 8.7% over the forecast period, due to increasing prevalence of chronic diseases. The market was valued at US$ 30.16 billion in 2023. Regional analysis indicates North America dominates the market currently due to favorable reimbursement policies and advanced healthcare infrastructure in the region. Key players operating in the anatomic pathology market are Thermo Fisher Scientific, F. Hoffman-La Roche AG, Agilent Technologies, Danaher Corporation, Quest Diagnostics, Inc., Biocartis NV, and Sakura FineTechnical Co., Ltd. Read More: https://www.ukwebwire.com/the-anatomic-pathology-market-incorporate-high-demand/  The Solar Water Pump Systems Market is estimated to be valued at US$ 1.92 billion in 2022 and is expected to exhibit a CAGR of 13% over the forecast period 2022-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Solar water pump systems use solar photovoltaic panels to power water pumps, which are mainly used for agricultural irrigation in remote off-grid locations where grid electricity is unavailable or very costly. With no fuel requirements and minimal operational costs once installed, solar water pumps provide a cost-effective and sustainable solution for reliable irrigation in agricultural fields. The components usually include PV modules, DC motor pump, controller, and civil work. Market Dynamics: Growing agricultural water demand, especially in arid and semi-arid regions, is expected to be a major growth driver for the solar water pump systems market over the forecast period. According to a study, the agricultural sector accounts for approximately 70% of the global freshwater withdrawals. The increasing scarcity of water resources coupled with growing population is necessitating efficient water management solutions. Additionally, the growing deployment of solar photovoltaic systems owing to supportive government policies and declining solar technology costs is boosting the adoption of solar water pumps worldwide. For instance, governments of many countries provide capital subsidies for installation of solar irrigation pumps to support farmers and incentivize the use of renewable energy. However, high initial installation costs remain a major barrier, especially in developing economies. Segment Analysis The global Solar Water Pumps Market Share is dominated by the submersible solar water pumps segment which holds around 60% share of the market. This is because submersible solar water pumps can be installed underground and are more durable than surface solar water pumps. They are also not affected by wind or weather and can draw water from deeper sources compared to surface pumps. PEST Analysis Political: Many governments across the world are providing subsidies and promoting solar energy usage which is driving the growth of the solar water pump systems market. Economic: The declining cost of solar components is making solar water pumps more affordable. This is encouraging farmers and households to switch to solar pumps for irrigation and other needs. Social: Growing awareness about renewable energy and its benefits such as lower operating costs and carbon footprint reduction is positively impacting the demand for solar water pump systems. Technological: Advancements in solar panel efficiency and battery technology have enhanced the performance of solar water pumps. Remote monitoring technologies are also being integrated for performance monitoring and automation. Key Takeaways The global solar water pump systems market is expected to witness high growth, exhibiting a CAGR of 13% over the forecast period of 2022-2030, due to increasing support from government policies and growing awareness about renewable energy sources. The market size is projected to reach US$ 3.48 billion by 2030 from an estimated US$ 1.92 billion in 2023. The Asia Pacific region is expected to dominate the market during the forecast period. This is attributed to large solar energy production and rapid rural electrification programs underway in countries such as India, China, and Japan. India accounts for over 40% of the global market owing to the government's initiatives to provide electricity to all households by 2023. Key players operating in the solar water pump systems market are Grundfos, Lorentz, Shakti Pumps, CRI Pumps, Tata Power Solar, Bright Solar, USL, Lubi Electronics, Solar Power & Pump Co, JNTech, JISL, ADA, Hanergy, CRI Pump, Dankoff Solar, Greenmax Technology, Rainbow Power Co, SunEdison, Solartech, Megha Engineering. These players are focusing on developing efficient and durable solar pumps with advanced monitoring and automation capabilities. Read More: https://www.ukwebwire.com/solar-water-pump-systems-market-is-estimated-to-witness-high-growth/  The dental implants market is estimated to be valued at US$ 5,049.7 million in 2023 and is expected to exhibit a CAGR of 6.5% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Dental implants are artificial roots that are surgically placed into the jaw to hold replacement teeth or dentures. They function similar to natural tooth roots by fusing securely with the jawbone over time. Dental implants have become a popular treatment option for replacing missing teeth as they look and feel more natural and stable compared to other alternatives such as dentures. The global market is driven by the increasing adoption of dental implants for tooth replacement and growing dental tourism in countries such as India, Hungary, and Turkey. Market Dynamics: The dental implants market is estimated to witness high growth over the forecast period owing to a rapidly growing geriatric population worldwide and the rising preference for dental tourism. As per the UN statistics, the population aged over 60 years is projected to double from 12% to 22% between 2015 and 2050. As tooth loss is common amongst the elderly, the demand for tooth replacement treatments including dental implants is expected to surge significantly. Furthermore, countries such as India and Turkey have emerged as highly-preferred dental tourism destinations owing to availability of equally effective treatment at significantly lower costs. For instance, the cost of a single dental implant surgery in India can be 5-7 times lower than Western countries such as the U.S. or the U.K. Lastly, advancements in dental implant designs and surface technology have improved success rates and longevity of implants, thus boosting market growth. Segment Analysis The Global Dental Implants Market is segmented into product type and material. Based on product type, the market is classified as dental titanium implants, zirconium dental implants and others. Among these, the titanium dental implants segment held the largest market share in 2021 owing to their high biocompatibility, high corrosion resistance and mechanical strength. Based on material, the market is bifurcated into titanium implants and zirconium implants. The titanium implants dominate the market with around 70% share due to their relatively lower cost and better osseointegration properties. PEST Analysis Political: The favorable government policies and regulations supporting the dental implants procedures across major countries is driving the market growth. For instance, the US government provides reimbursements for dental implant surgeries under Medicare. Economic: Rising disposable income and growing medical tourism in emerging nations are fueling the demand for cosmetic dental procedures involving dental implants. Social: Increasing social acceptance of cosmetic dental treatments along with the rising focus on dental aesthetic appearance among population is positively impacting the market. Technological: Advancements in digital dentistry, computer-aided implant treatment planning and robotic-guided implant surgery solutions have simplified the implant placement procedures boosting the adoption. Key Takeaways The global dental implants market size is expected to reach US$ 5,049.7 million in 2023, growing at a CAGR of 6.5% during the forecast period. The high growth can be attributed to the increasing number of tooth loss cases owing to rising incidence of dental caries and periodontal diseases. Regional analysis: North America dominated the global market in 2021 and is expected to maintain its lead over 2023-2030 due to rising dental expenditure and availability of advanced treatment options in the region. Key players: Key players operating in the dental implants market are DENTSPLY Implants, Straumann AG, Bicon Dental Implants, Anthogyr, KYOCERA Medical Corporation, Lifecore Dental Implants, Zest Anchors, Implant Innovations Inc, BioHorizons IPH, Inc., Neobiotech USA. Inc., Sweden & Martina, TBR Implants Group, Global D, and MOZO-GRAU, S.A. Read More: https://www.rapidwebwire.com/dental-implants-market-size-and-share  The transcranial magnetic stimulator market is estimated to be valued at US$ 638.4 Mn in 2023 and is expected to exhibit a CAGR of 12.4% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Transcranial magnetic stimulator (TMS) is a non-invasive technique used for stimulating small areas of the brain by means of focussing intense and brief magnetic field impulses on the region of interest. The device consists of a stimulating coil, which produces short magnetic pulses when electric current is passed through it. It is generally used in treatment of neuropathic disorders such as major depressive disorder, schizophrenia, addiction disorders, Alzheimer's disease and Parkinson's disease among others. TMS therapy is gaining popularity as an alternative to pharmacological and surgical treatments owing to its safety and effectiveness. Market Dynamics: Rising prevalence of neuropathic disorders across the globe is a key driver augmenting growth of the TMS market. According to WHO, around 450 million people suffer from such disorders globally. In addition, improving accessibility of TMS devices major healthcare facilities worldwide is expected to boost adoption. Moreover, increasing R&D investments by manufacturers in development of innovative and portable TMS devices is anticipated to offer lucrative opportunities over the forecast period. However, high costs associated with TMS procedures and lack of trained professionals may limit market growth to some extent. Segment Analysis The global Transcranial Magnetic Stimulator Market Size is divided into three key segments based on application - Diagnostics & Research, Therapy, and Others. Among these, the Therapy segment currently dominates with the largest market share owing to the increasing usage of rTMS technology for the treatment of various neurological and psychiatric disorders such as depression. This non-invasive therapy has shown positive results and fewer side effects as compared to medication. PEST Analysis Political: Governments across various countries are supporting the use of alternative treatment options for mental health disorders due to growing awareness. They are approving policies to promote the adoption of novel medical devices like TMS. Economic: The rising healthcare expenditure to deal with the growing prevalence of neurological conditions and the presence of favorable reimbursement schemes are fueling the market growth economically. Social: Growing social acceptance of brain stimulation therapies and reductions in stigma associated with mental illnesses are propelling their demand. Technological: Continuous R&D investments by players have led to rapid technological advancements in TMS devices. The introduction of multi-coil rTMS devices and devices integrated with neuronavigation systems has further widened their clinical applications. Key Takeaways The global Transcranial Magnetic Stimulator market size is expected to reach US$ 638.4 Mn in 2023, expanding at a high CAGR of 12.4% during 2023 - 2030. The growth can be attributed to the rising geriatric population who are prone to neurological disorders and increasing adoption of rTMS for mental health conditions. Regionally, North America captures the highest market share currently owing to advanced healthcare infrastructure and rising prevalence of neuropsychiatric diseases in the region. However, Asia Pacific is expected to witness the fastest growth over the forecast period backed by improving access to novel brain stimulation therapies and growing medical tourism in the region. Key players operating in the Transcranial Magnetic Stimulator market are Magstim, Brainsway, Nexstim, Neuronetics, Remed, Yiruide, Dr. Langer Medical, MAG & More, Deymed, MagVenture, eNeura, Neurosoft, Neuro-Electrics, TCT Research, MagPro Compact, Axilum Robotics, Onward Medical and Rogue Resolutions. They are focusing on new product launches, geographical expansions and strategic collaborations to strengthen their market presence. Read More: https://www.rapidwebwire.com/transcranial-magnetic-stimulator-market-demand/  The Flow Computers Market is estimated to be valued at US$ 679.5 Million in 2023 and is expected to exhibit a CAGR of 9.6% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: A flow computer is an embedded system that measures, monitors and controls flowmeters for liquid and gas transfer and transactions across pipelines and production networks. It performs calculations based on flow meter signals and other process variables to determine flow rate, volume, mass, energy, density, and other flow quantities. Flow computers are widely used in the oil & gas industry for custody transfer applications such as oil and natural gas production allocation, inventory control, and well allocation. Market Dynamics: The global flow computers market is expected to witness significant growth over the forecast period owing to increasing oil & gas production activities around the world and rising need for flow monitoring and measurement solutions. According to BP's Statistical Review of World Energy 2021 report, global oil production increased by around 5.8 million barrels per day (mb/d) from 2019 to 2020. For natural gas, the global production grew by around 70 billion cubic meters (bcm) from 2019 to 2020. This increasing production is generating high demand for advanced flow measurement solutions like flow computers for custody transfer, inventory control and other applications. Additionally, flow computers provide critical benefits like accurate measurement, data monitoring from remote locations, automated operations and detection of leaks or anomalies. These benefits are further fueling the demand for flow computers across industries. However, high installation and maintenance cost of flow computers may hamper market growth over the forecast period. Segment Analysis The global Global Flow Computers Market is segmented on the basis of component, connectivity, operation, industry vertical and geography. The component segment is further divided into hardware, software and services. Among these, the hardware segment dominated the market in 2022 owing to the increasing demand for process flow computers, ultrasonic flow meters and other primary elements for flow computing and measurement. PEST Analysis Political: Flow computers are used across key industries such as oil & gas, energy & power, chemicals, water & wastewater treatment, food & beverages and others. Supportive government policies encouraging adoption of digital technologies across industries are positively impacting the demand. Economic: Increasing investments in digital transformation initiatives, stable economy and rising spending power are driving the growth of flow computers market. Social: Need for optimization of resources with minimum environmental impact is augmenting the adoption of flow computers for inventory management and custody transfer applications. Technological: Advancements in connectivity capabilities, real-time data analytics, predictive maintenance solutions and integration with industrial internet of things are offering new opportunities. Key Takeaways The global Flow Computers market is expected to witness high growth, exhibiting CAGR of 9.6% over the forecast period 2023 - 2030, due to increasing demand from oil & gas industry for allocation management, custody transfer and inventory management. Regionally, North America dominated the market in 2022 owing to robust presence of key players and growth in shale gas exploration and production activities in the region. Regional analysis Regionally, North America dominated the market in 2022 due to robust presence of key players like Emerson Electric Co., ABB Ltd., Schneider Electric SE and Honeywell International Inc. in the US and Canada and growth in shale gas exploration and production activities. Asia Pacific is expected to witness fastest growth during the forecast period owing to increasing oil & gas upstream and downstream activities in major economies like China, India and Indonesia. Key players Key players operating in the Flow Computers market are Emerson Electric Co., ABB Ltd., Thermo Fisher Scientific Inc., Yokogawa Electric Corporation, Schneider Electric SE, Honeywell International Inc., Siemens AG, Badger Meter Inc., AMETEK Inc., Equinor ASA, KT-Flow, KROHNE Group, OMNI Flow Computers Inc., Schlumberger Limited, SICK AG, Logic Beach Inc., Flowmetrics Inc., Contrec Ltd., Kessler-Ellis Products Co., TechnipFMC plc. Read More: https://www.rapidwebwire.com/flow-computers-market-demand/ Space Capsule Market Set to Surge Driven by Private Space Initiatives and Improving Accessibility10/31/2023  The Space Capsule Market is estimated to be valued at US$ 4.73 Billion in 2023 and is expected to exhibit a CAGR of 12.6% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: A space capsule refers to a crewed spacecraft that has a rounded, somewhat streamlined shape for reentry into the Earth's atmosphere. Space capsules are used to carry astronauts or passengers into low Earth orbit or beyond. Some key manufacturers of space capsules include SpaceX, Boeing, Sierra Nevada Corp., Lockheed Martin, Northrop Grumman, Blue Origin, and Virgin Galactic. These companies are working to develop reusable space capsules to reduce the costs of space travel and make it more accessible to common people. Market Dynamics: The space capsule market is expected to witness significant growth over the forecast period, driven by increasing private space initiatives aimed at space tourism. Various companies such as SpaceX, Blue Origin, and Virgin Galactic are aggressively investing in the development of space capsules to carry paying passengers on suborbital flights. This is expected to boost the demand for space capsules over the coming years. Additionally, many national space agencies are collaborating with private players to commercialize low Earth orbit, which is also likely to create growth opportunities for space capsule manufacturers. Furthermore, development of reusable space capsules is another major driver as it helps reduce the payload costs substantially, thereby improving the accessibility of space travel. For instance, SpaceX's Dragon capsule is designed to be reusable upto 10 times which is a key factor behind the rapidly falling costs of launches. Segment Analysis The global Space Capsules Market Demand is dominated by the orbital capsule segment. Orbital capsules are specialized vehicle or spacecraft that transport crew or cargo from a launch vehicle to an orbiting space station. Orbital capsules are specifically designed to withstand extreme temperature fluctuations during launch and re-entry into Earth's atmosphere. Advantages like high payload capacity and reusable features have made orbital capsules a popular choice in the space industry. PEST Analysis Political: Space capsule development projects receive strong government support and funding as they are crucial for national space agencies. Favorable space policies and regulations encourage private sector investments. Economic: Growing satellite deployment services and space tourism industry are driving sales in the space capsule market. Developing economies are increasing their space budgets to become self-reliant in space technology. Social: Rising enthusiasm among the general public for commercial space flights is positively impacting the market. Demand is increasing for sub-orbital and orbital space tourism services. Technological: Advancements in heat shield technology, electronics miniaturization, and 3D printing are allowing design of optimized and reusable space capsules. Developments in reusable rockets will further stimulate the commercial space market. Key Takeaways The global space capsule market size is expected to witness high growth, exhibiting a CAGR of 12.6% over the forecast period of 2023-2030, due to increasing commercial spaceflight activities. The market was valued at US$ 4.73 Billion in 2023. The North American region dominates the space capsule market with the largest number of orbital launches. Major space agencies and private spaceflight companies based in the US are driving significant demand. Robust government spending to support nationally important space initiatives have made North America the fastest growing regional market. Key players operating in the space capsule market include SpaceX, Boeing, Sierra Nevada Corp., Lockheed Martin, Northrop Grumman, Blue Origin, Virgin Galactic, Exos Aerospace, Firefly Aerospace, ULA, Rocket Lab, Vector Launch, Orbex, Relativity Space, Arianespace, IHI Aerospace, Mitsubishi Heavy Industries, Dynetics, Energia, and Thales Alenia Space. SpaceX has established itself as the leader with its focus on reusable orbital capsules like Crew Dragon and planned projects like Starship. Read More: https://www.rapidwebwire.com/space-capsule-market-growth-and-demand/  The preterm birth and prom testing market is estimated to be valued at US$ 1.69 billion in 2023 and is expected to exhibit a CAGR of 12.5% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Preterm birth and prom testing help identify women who are at high risk of preterm birth. Preterm birth is defined as any birth before 37 weeks of gestation. Preterm birth complications are the leading cause of death among children under 5 years of age, globally. Prom testing measures the level of fetal fibronectin (fFN) in cervicovaginal secretions, which increases as the pregnancy progresses towards parturition. Negative fFN results help reassure a patient that delivery is not imminent, avoiding unnecessary interventions. Market Dynamics: The preterm birth and prom testing market is driven by increasing acquisitions and collaborations between key players. For instance, in May 2022, Medix Biochemica acquired Sera Prognostics, a leading innovator in clinical diagnostics for early prediction of preterm birth. This acquisition strengthens Medix Biochemica's position in preterm birth prediction testing. Abbot Laboratories has also launched a new point-of-care test for assessing the risk of preterm birth. Detecting fFN levels, the new test delivers lab-accurate results in just 10 minutes, allowing faster clinical decisions. These initiatives will help expand testing volumes as well as adoption rates globally over the forecast period. Additionally, rising preterm birth rates around the world propel the need for preterm birth and prom testing. According to WHO, preterm birth complications account Segment Analysis The Global Preterm Birth And Prom Testing Market is segmented into diagnostic devices and assays. The diagnostic devices segment dominated the market in 2022 due to the increasing demand for portable ultrasound monitors to diagnose preterm birth at early stages. These portable ultrasound monitors provide quick results with high accuracy, which has increased their adoption among healthcare professionals. PEST Analysis Political: The governments in various countries are investing heavily to create awareness among women regarding risks of preterm birth and the availability of diagnostic tests. This is expected to boost the market growth. Economic: The rising per capita healthcare expenditure provides ample growth opportunities for players in this market. Additionally, reimbursements for prom tests are supporting the market expansion. Social: The increasing health consciousness among people and growing acceptance of modern diagnostic techniques for preterm birth testing is fueling the market demand. Technological: Continuous innovations are helping market players to develop rapid, accurate, and portable diagnostic devices for early detection of preterm birth. Advances in assay procedures are also augmenting the market. Key Takeaways The global preterm birth and prom testing market is expected to witness high growth, exhibiting a CAGR of 12.5% over the forecast period, due to increasing awareness about availability of diagnostic tests and risks of preterm birth. The U.S. dominates the market currently due to increasing healthcare expenditure, advanced healthcare infrastructure, and high adoption of modern diagnostic techniques for preterm birth. Favorable reimbursement policies are also supporting the market growth in the region. Regional analysis The Asia Pacific region is projected to grow at the fastest pace during the analysis period. This can be attributed to growing population, improving access to healthcare facilities, rising healthcare expenditure, and increasing focus of market players on tapping growth opportunities in emerging Asian countries. Key players Key players operating in the preterm birth and prom testing market are Abbott Laboratories, Biosynex, Qiagen Sciences LLC, Clinical Innovations LLC, Sera Prognostics, The Cooper Companies Inc., Medixbiochemica, Hologic Inc., IQ Products, NX Prenatal Inc., Promega Corporation, Medical Predictive Technologies Inc., Biosynex, Clinical Innovations LLC, NX Prenatal Inc., Medixbiochemica, Qiagen Sciences LLC, Sera Prognostics Inc., Insight Pharmaceuticals LLC, Creative Diagnostics. Read More: https://www.rapidwebwire.com/preterm-birth-and-prom-testing-market-scope/  The vortex turbine market is estimated to be valued at US$ 102.6 million in 2023 and is expected to exhibit a CAGR of 11.5% over the forecast period 2023-2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Vortex turbines utilize kinetic energy generated from gases to produce electricity. These turbines are self-starting, have simple design with fewer moving parts and can sustain high winds. They are suitable for various applications such as water & tidal energy, power generation from waste streams, and distributed energy generation. Vortex turbines offer advantages of low cost, easy maintenance and ability to generate energy from low head sites which makes them viable alternative to conventional turbines. Market Dynamics: The growth of the global vortex turbine market is driven by increasing demand for renewable energy sources as well as need for cost effective technologies. Energy production from renewable sources has gained prominence in recent years to mitigate environmental impacts of fossil fuel usage. Vortex turbines can harness power from low velocity gases and waste streams without requiring dams or water reservoirs like conventional hydroelectric systems. Their simple design makes installation and maintenance economical. Furthermore, ability to generate electricity from sites with low head drops expansion of viable locations for energy production. Vortex turbines are well-suited for small scale distributed power applications. The growing decentralized energy requirement from rural areas and off-grid sites will further support market growth over the forecast period. Segment Analysis The Global Vortex Turbine Market is dominated by the bladeless vortex turbine segment which accounts for over 40% market share. This is because bladeless vortex turbines do not have any moving parts like blades which reduces maintenance costs significantly. They can last over 25 years with almost zero maintenance. This provides an edge over traditional bladed turbines. PEST Analysis Political: Governments across regions are introducing supportive policies and regulations to promote renewable energy adoption. They offer various subsidies and tax incentives for installations of vortex turbines. Economic:The cost of generating power from vortex turbines is much lower compared to fossil fuels. Their operating costs are very low as they don't have any major overheads like blade replacements. Social: There is a growing demand for greener sources of energy due to increasing environment degradation concerns. Vortex turbines are more socially accepted as they don't produce any noise or disturb bird migration patterns. Technological: Continuous research and development is underway to enhance efficiency and power outputs of vortex turbines. New designs optimized for various water levels are being developed. Many startups are also working on designs that can tap low speed breezes and marine currents better. Key Takeaways The global vortex turbine market is expected to witness high growth, exhibiting CAGR of 11.5% over the forecast period, due to increasing demand for renewable sources of energy. The market size is projected to reach US$ 302 billion by 2030. North America dominated the market in 2023 with a share of over 30%, led by U.S. and Canada owing to supportive policies and presence of key players in the region. Asia Pacific is expected to be the fastest growing market, growing at a CAGR of 12.5% during the forecast period with China and India emerging as major markets. Key players operating in the vortex turbine market are TurboTech Ltd, Vortex Energy Solutions, Future Blades, Green Energy Solutions, TurbineTech, Aerodyn, ArborWind, Urban Green Energy, Vortec Energy Systems, WindStax, Earth Mill, Vortex Bladeless, Sauer Energy, Calnetix Technologies, Enertime, Qnergy, Exro Technologies, Oscilla Power, Vortex Hydro Energy, Quantum Vortex Turbines. These players are focusing on manufacturing advanced designs of vortex turbines with higher efficiencies and power outputs to tap into new application areas. Read More: https://www.rapidwebwire.com/vortex-turbine-market-demand/  The Japan Fashion Ecommerce Market is estimated to be valued at US$ 56.03 Bn in 2023 and is expected to exhibit a CAGR of 12.5% over the forecast period 2023 - 2030, as highlighted in a new report published by Coherent Market Insights. Market Overview: Fashion ecommerce in Japan enables consumers to shop for clothing, footwear, accessories and other fashion products online from various domestic and international brands. Ecommerce businesses in Japan offer a wide variety of fashion products through their websites and mobile apps along with value-added services like fast delivery, easy payment options and cash-on-delivery. This has made online fashion shopping more convenient for consumers in Japan. Market Dynamics: The growth of the Japan Fashion Ecommerce Market is primarily driven by the increasing adoption of smartphones and proliferation of high-speed internet across Japan. Over 96% of the Japanese population now has access to smartphone and internet which has significantly boosted online shopping activities in recent years. Moreover, the COVID-19 pandemic has further accelerated digital adoption as more people turned to online platforms for shopping during lockdowns and social distancing periods. The Japanese government encouraging initiatives to promote cashless payments have also facilitated growth of digital commerce. However, preference for physical store experience among older demographic and lack of product touch and feel in online shopping limit the market potential to a certain extent. Segment Analysis The Japan Fashion Ecommerce Market Size is dominated by the women's fashion segment. It accounts for nearly 35-40% of the overall market revenues as Japanese women are heavily invested in the latest fashion and clothing trends. They frequent online shopping portals multiple times a week to check for new arrivals and deals. The men's fashion segment generates around 25-30% of sales due to rising health consciousness and demand for comfortable yet trendy wear. PEST Analysis Political: A stable political landscape and supportive government policies have encouraged entrepreneurship and digitization in Japan. Economic: Japan has a highly developed free market economy. Rising income levels and exposure to global fashion have boosted online spending on clothes and accessories. Social: Younger population is technology savvy and adaptive to new brands. Shift towards nuclear families and dual-income households has increaseddemand for convenience in shopping. Technological: High smartphone and internet penetration along with fast broadband connectivity have enabled customers to browse and purchase merchandise online efficiently across diverse platforms. Key Takeaways The Japan fashion ecommerce market size is valued at US$ 56.03 Bn in 2023 and is expected to grow at a CAGR of 12.5% during 2023 - 2030. Rapid adoption of smartphones and increasing preference of customers towards online shopping are expected to drive the market in the forecast period. Regional analysis indicates that Tokyo, Osaka, and Aichi are the leading regions in terms of online apparel spending in Japan. The surge is attributed to the digitally connected, affluent population residing in major cities. Key players operating in the Japan fashion ecommerce market are JAPANNET Shopping, Happy Mail, LOHACO, SHOPLIST, iStyle by Cosme.net, DMM.com, WEGO, Felissimo, Rakuten, Amazon Japan, Zozotown, Yahoo! Shopping, @cosme, Winc, TRADEMARK JAPAN, CaSa, SHOP JAPAN, Felisiya, dot-st, LOFT. Players like Rakuten, Zozotown and Amazon have captured substantial market share over the years. Read More: https://www.rapidwebwire.com/japan-fashion-ecommerce-market-demand/ |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

December 2023

Categories |

RSS Feed

RSS Feed